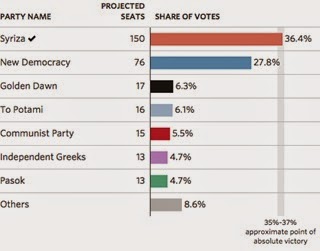

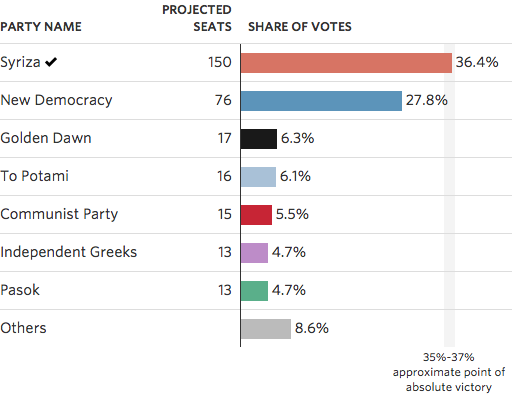

The large victory of the Syriza party in Greece, with Tsipras just

one seat below absolute majority (see Table 1 below) raises the questions

:”What will happen now in the Eurozone? Is a Grexit scenario

possible?”My take here is that not much is likely to happen, except some

tough bargain between the new government and the Troika. Let’s consider the

following points:

one seat below absolute majority (see Table 1 below) raises the questions

:”What will happen now in the Eurozone? Is a Grexit scenario

possible?”My take here is that not much is likely to happen, except some

tough bargain between the new government and the Troika. Let’s consider the

following points:

Table 1: Election Results

{kind=link}

- No one, neither the new government of

Greece nor the Troika, can credibly threat to “overturn the

table”, abandon negotiations and let Greece exit the Euro. This

outside option would be too costly for both parties. Greece has financing

needs of about 25 billion in the next two years (IMF Fiscal Monitor, October

20014) and has no access to capital

markets. A disorderly default on official debt would cut off Greek banks

from collateralized lending from the ECB, and would likely result in

a dangerous banking and currency crisis. On the other hand, a Grexit

would send shock waves through the Eurozone: markets may once again

price exchange rate and default risks in peripheral countries’ (e.g.

Italy) sovereign debt, jeopardizing the financial stability of the

area as a whole. - If negotiations have to be, the question is: on

what will they be? It is unlikely that a consistent debt restructuring can

be agreed upon, for three reasons. First, after PSI in 2012,

official creditors who now hold about 83% of Greek debt have already

granted large extensions of debt maturity (the average is 16.5 years (1),

compared to about 7 in Italy) and have considerably reduced interest

rates. With a debt to GDP ratio above 175%, Greece pays about 4.5%

of GDP in interests, less than Italy does, with 134%. Taking into account

that interests on ECB’s debt holdings

flow back to Greece, the rate falls to less than 3% (2). Second, a

restructuring would prompt similar requests from other peripheral EU

debtor countries, opening up a Pandora’s box. Finally, the German

electorate does not want to hear about debt forgiveness.

It is more likely

that negotiations will concern giving more time for fiscal adjustment.

Although the new guidelines (3) for the Stability and Growth pact,

similarly to Draghi’s QE, do not apply to Greece, some leeway could be

made invoking the “cyclical clause”, that reduces fiscal

adjustment when the (negative) output gap is very large. Consider

that Greece has made an unprecedented fiscal adjustment in recent years

(see graph below), with a primary structural balance moving from -13.6% of

GDP in 2011 to +5.4 % today, thus concessions may be easier to

justify.

Figure 1:

Cyclically Adjusted Primary Balance

(% Potential Output), IMF Data Mapper

Cyclically Adjusted Primary Balance

(% Potential Output), IMF Data Mapper

{kind=link}

Now assume that Tsipras and Merkel bargain on the size of the

discount on the fiscal adjustment. How much is Tsipras going to get? A simple

back-of-the envelope calculation may help here.

If we use Rubinstein (4) sequential bargaining approach, with Tsipras and

Merkel making alternative offers and deciding to accept or reject, the answer

depends how patient are the two sides. It turns out that each side’s gets a

larger share of the pie the more “patient” she/he is, and the more

“impatient” is the opponent. The reason is that one can make a lower

offer/counter-offer to an impatient opponent.

Table 2 below plots Tsipras’ equilibrium pay-off, the reduction in required

fiscal adjustment as a percentage of output, for different values of the

discount factors of the two sides. As the Troika becomes more

impatient, its discount factor (d2) falls, by moving from left to right in the

table. Tsipras becomes more impatient (d1 falls) by moving

downwards.

discount on the fiscal adjustment. How much is Tsipras going to get? A simple

back-of-the envelope calculation may help here.

If we use Rubinstein (4) sequential bargaining approach, with Tsipras and

Merkel making alternative offers and deciding to accept or reject, the answer

depends how patient are the two sides. It turns out that each side’s gets a

larger share of the pie the more “patient” she/he is, and the more

“impatient” is the opponent. The reason is that one can make a lower

offer/counter-offer to an impatient opponent.

Table 2 below plots Tsipras’ equilibrium pay-off, the reduction in required

fiscal adjustment as a percentage of output, for different values of the

discount factors of the two sides. As the Troika becomes more

impatient, its discount factor (d2) falls, by moving from left to right in the

table. Tsipras becomes more impatient (d1 falls) by moving

downwards.

Table 2: Tsipras’ Payoff

|

Author

calculations based on Rubinstein (1982) |

Since Tsipras faces a higher interest rate and political pressure than Merkel,

the solution is likely to lie below the principal diagonal of the pay-off

matrix. My best guess is that the equilibrium solution will be a number close

to 25%, which means that rather than running a structural primary surplus

of the order of 5 % of potential output, as envisaged in the IMF projection

(see Figure 1 above), Tsipras could get away with a number close to 3.75 % .

Just some breathing space.

the solution is likely to lie below the principal diagonal of the pay-off

matrix. My best guess is that the equilibrium solution will be a number close

to 25%, which means that rather than running a structural primary surplus

of the order of 5 % of potential output, as envisaged in the IMF projection

(see Figure 1 above), Tsipras could get away with a number close to 3.75 % .

Just some breathing space.

Footnotes

1.

(1) F.Giuliano, Financial Times

Jan 25, 2015, http://www.ft.com/intl/cms/s/0/6e5532c0-a310-11e4-ac1c-00144feab7de.html#axzz3Q1bm0Lx3

(1) F.Giuliano, Financial Times

Jan 25, 2015, http://www.ft.com/intl/cms/s/0/6e5532c0-a310-11e4-ac1c-00144feab7de.html#axzz3Q1bm0Lx3

(2) Zsolt Darvas, 2015, “Greek choices after the

elections”, Bruegel http://www.bruegel.org/nc/blog/detail/article/1551-greek-choices-after-the-elections

(3) Paolo

Manasse, 2015, “The EU new fiscal flexibility guidelines: an assessment”,

forthcoming voxeu.org and http://paolomanasse.blogspot.it/2015/01/the-eu-new-fiscal-flexibility.html

4. (4) Ariel Rubinstein, “Perfect Equilibrium in a Bargaining Model,” Econometrica, 50(1982), 97-109.