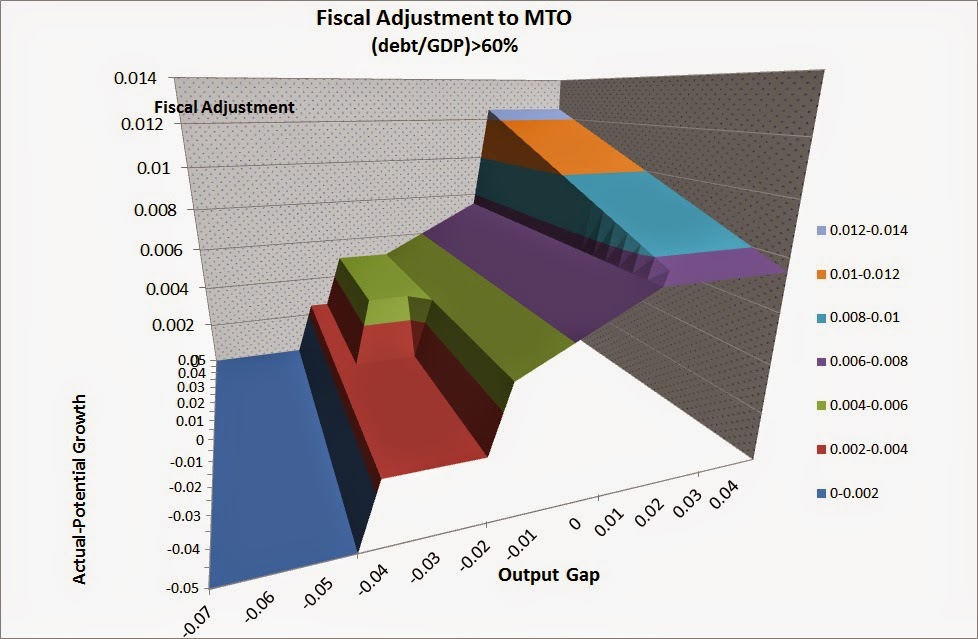

I have discussed here the “new” guidelines on the Stability and growth pact (SGP) issued on January 13 by the European Commission. As many economist, I really enjoy “seeing” things on a graph. So here is the “new” SGP in 3D . On the vertical axis I plot the fraction of GDP a country will be required to tighten in order to reach the so called “medium term objective”(MTO), as a function of the output gap, from left to right, and of the difference between the actual and the potential growth, the width of the box, from down upwards.

To draw the box I made a few assumptions, for example I that the fiscal adjustment rises linearly between “normal” and “good times”. I also assumed that growth is negative only when the output gap is below -4% so that I can ignore the condition on negative growth (unfortunately I cannot plot a graph in 4D).

The picture refers to countries with debt GDP ratio in excess of 60% (most of EU members).

The fiscal effort rises as the economy improvese (as we move from left to right) and as the difference between the actual and potential growth rates becomes positive (as we move up)

So what do we learn?

First, when the output gap times leaves “exceptionally bad times”, above the value of -4%, we have a first hike in the fiscal adjustment , from 0 to .25% of GDP. Moreover, as soon as we enter “normal times”, a gap between -1.5 and +1.5%, the fiscal adjustment jumps up even more. Actually the fiscal effort starts rising even before, in “bad times” when the gap is between -3 and -1.5%, provided the difference between actual and potential growth has turned positive. Finally, in good times, a gap above 1.5%, the size of the step increases rapidly with the excess growth over potential.

Thus even under the new interpretation, the SGP confirms to be quite restrictive, and the step-wise nature of the fiscal rule implies that very similar cyclical conditions may be treated with very different doses of austerity, which is hard to justify.

Will this complicated scheme ensure debt sustainability? Not necessarily, of course: the latter depends on nominal rates, inflation, real GDP growth and the debt/GDP ratio, rather than on the EU calculations of output gaps and potential growth….