(by Paolo Manasse and Giulio Trigilia)

Since the financial crisis began in 2008, economists have been warning of a nightmare scenario, one that is now unfolding in the European Union: a domino effect, as the economies of Greece, Ireland, Portugal, Spain, and Italy (the PIIGS, as they’ve come to be known) collapse. Yet most observers got the ordering wrong: the crisis arrived in Italy before Spain.

The reason is political: Spanish Prime Minister José Luis Rodríguez Zapatero, realizing he had lost the political backing necessary for difficult reforms, announced last April that he would not run for reelection. Silvio Berlusconi, who faced similar economic challenges, tried to keep his seat. He lost that battle when he resigned on Saturday, after having let the Italian economic crisis fester for months. Ultimately, financial markets and the specter of a default dethroned the sultan (1)

We have argued on Vox (2) that the current Italian troubles are largely homemade, they are not the result of contagion from Greece, so that weak economic fundamentals, more than Berlusconi’s lack of credibility, are key (3). This is why financial markets, after a brief toast, have not rallied when President Napolitano asked Professor Monti to form a new government. The spread of BTPs is still at 500 points and the Italian Treasury just sold 3 billion 5-year bonds at a yield of 6.29%, almost one percentage point higher than in October. Monti’s task will be a formidable one: he will need the support of a recalcitrant and bitterly divided Parliament to pass painful reforms.

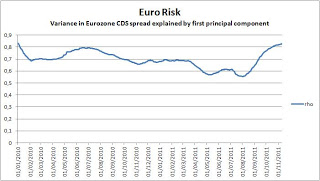

This column argues that after period of “risk decoupling”, with markets increasingly discriminating between European sovereigns, we are now back to the era of “Euro-risks”. In other words, financial markets are pricing in the notion that an Italian collapse, given the huge amount of debt involved (1.9 trillion) and its wide circulation (about 44 percent held by non residents), would mean the end of the Euro and would not leave anyone unscathed. We offer three pieces of evidence (click on figures to enlarge)

1. Euro Risk

|

| Fig1. Source: authors’ calculations on Data Stream d |

|

| Fig. 2. Source: DataStream |

2. Country Correlations with EU-Risk

|

| Fig.3. Source: authors’ calculations on Data Stream data |

Next we look at the role played by each country-specific sovereign risk in the EZR risk. Figure 3 displays the “factor loadings” (the weights) of individual CDS sovereigns in the EZR. These weights answer the question: how correlated is country risk with Euro-wide risk? We can observe the following: first, as of may 2011 Greece, Portugal, and Ireland, the recipients of EU-IMF bailout loans, decoupled from the other countries, France Germany and Italy. Their falling weights suggest that they were becoming progressively “orthogonal” to the EZR: the risk of systemic contagion was limited. This is no longer the case. As of August 2011, however, they had a spectacular come back. Since these countries’ spread did not improve, this means that the “safer” countries increasingly worsened, as shown by the progressive rise in the Italian component.

3. Italy and other EZ countries

|

| Figure 4: Source: authors’ calculations on Data Stream data |

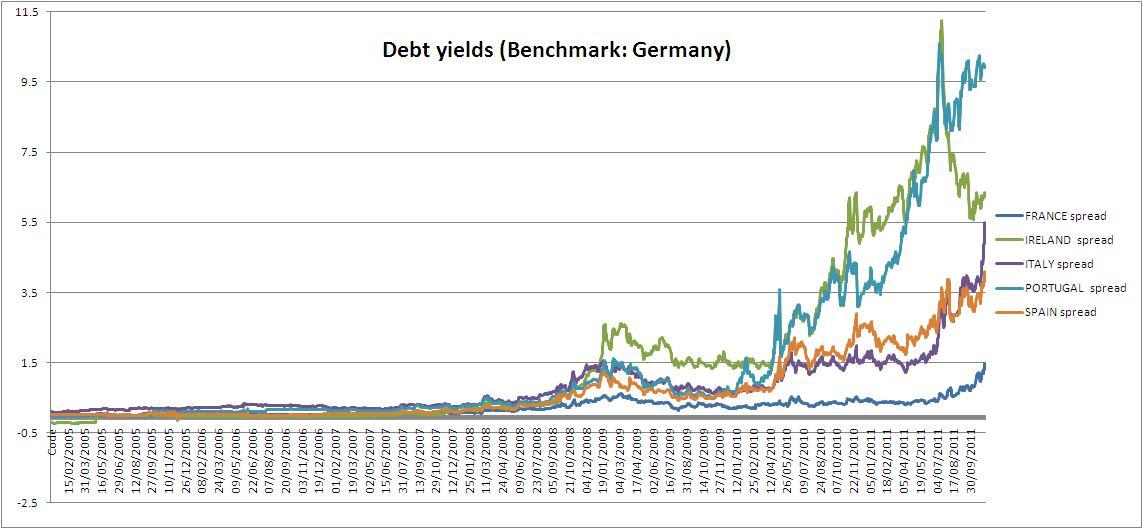

The last piece of evidence shows the evolution of the bilateral correlations between Italy’s and other countries’ sovereign risks (Figure 4). The co-movement with Ireland, Spain, Germany and Greece started to fall since October 2010, but from January 2011 it gradually climbed back close to unity (Ireland being the exception). As of today it seems that market perceive little diversification from investing in different EUZ countries.

Conclusions

The evidence from CDS sovereign spreads supports the view that markets once again are bundling Europeans all together, with Italy becoming the largest source of contagion and other sovereign bonds providing little diversification opportunities. If this trend continues and the Italian crisis does not find a solution, not only France‘s rating but Germany’s and the whole EUZ financial stability will be at risk. This is why Europeans (and the US) should exert the utmost pressure to make sure that the Monti experiment does not end in failure: what Italians will do for Italy, bad or good, they will do also for Europe.

Notes

(1) see Paolo Manasse, “Can Mario Monti Rescue Italy?” , Foreign Affairs, November 15, 2011

(2) Paolo Manasse and Giulio Trigilia, “The fear of Contagion in Europe” , Voxeu.org, 6 July 2011

(3) Paolo Manasse, “Credibility is not Everything”, Voxeu.org, 9 November 2011,