Low nominal interest on government bonds are good news, in that they slow down the dynamics of public debt and encorage spending.

Thus the recent auction of one-year government bonds (BOT) where the Italian Treasury was able to sell 7 billion worth of paper at a yield of 0.279%, down from the previous record low of 0.387%, and where the demand was twice the amount on offer, is an encouraging sign for the government.

Yet the real expected interest rate is much higher, given that expected inflation is negative (around -1.5%) This, together with flat disposable income and households’ borrowing constraints, is holding back consumption and demand.

The risk of the positive auction is to encourage further leniency of the government in carrying out the required economic reforms, by giving the illusion that the cost of borrowing is going to stay low.

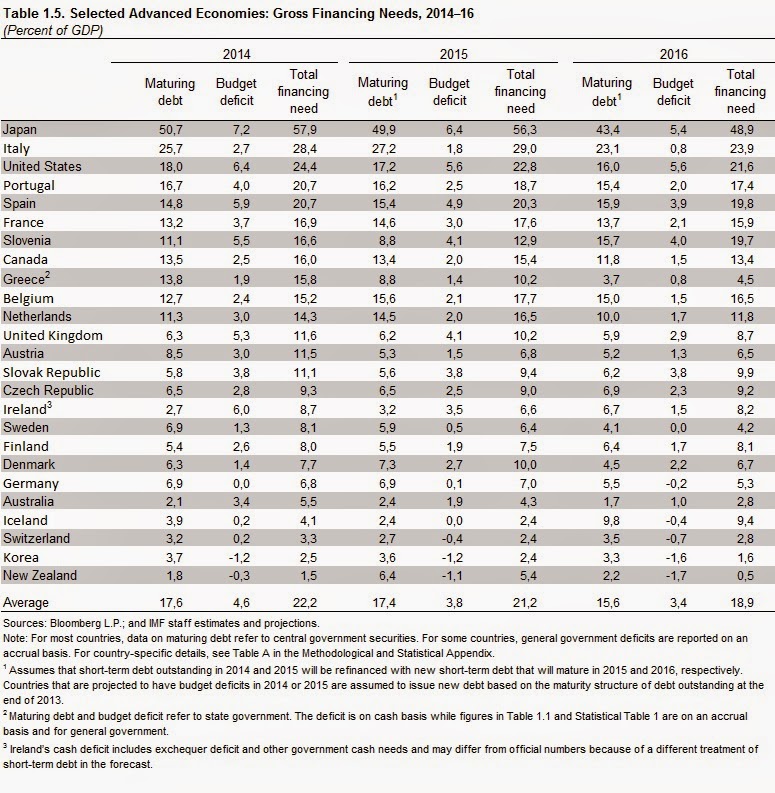

A look a the table above, from April 2014 IMF’s Fiscal Monitor, should dismiss any such complacency.

In 2015 the Italian gross financing needs, which sum up the borrowing requirements of the budget deficit and the maturing debt to be rolled over, will amount to almost one third of GDP, to fall to 24% in 2016.

Not really something on which one can rest on his laurels…