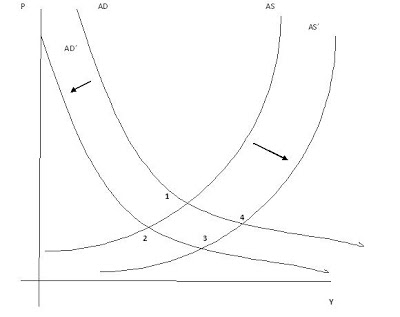

(from Economonitor, RGE, 2 Dec 2011) The program of fiscal consolidation + structural reforms that the Monti government is envisaging, in line with EU and OECD recommendations could be derailed by deflation + recession. The Aggregate Supply – Demand framework (AS-AD) in the figure helps making the simple point. Budget cuts (particularly tax hikes and expenditure cuts) depress demand, shifting the AD curve to the left, and moving the economy from the equilibrium point 1 to point 2, where output (Y) and the price level (P) fall. Over time, structural reforms shift the AS curve out to the right by liberalizing the market for goods and services as well as the labor market. In the short run however, demand may be negatively affected by these reforms as firms find it easier to fire workers and pensions are cut, depressing incomes and consumption, while stocks and real estate prices fall as a result of higher property are taxation. The AS curve shifts over time from equilibrium point 2 to 3, as the economy gradually improves. Note that while structural reforms help the economy out of the recession, they exacerbate the fall in prices. This is a big problem. Not only output and revenue temporarily fall as a result of fiscal consolidation, but prices keep falling overtime, possibly pushing up real interest rates if market continue to perceive sovereign bonds as risky. Deflation (and the temporary recession) therefore accellerate the the rise in the debt/GDP ratio.Here the solution is trying to push the economy towards point 4, but that ain’t easy. Expansionary fiscal policies are ruled out and the nominal exchange with the EU trade partners cannot be devalued if Monti wants to stay in the Euro. A little can be done by “fiscal devaulation”: by shifting the tax burden from employee contributions to VAT the givernment may engineer a fall in the relative price of domestic/ foreign goods so that competitiveness vis a vis the main EU trade partners improves, the general price level rises and hopefully so does foreign demand. Empirically this effect is likely to be small. More can be done by the ECB via a strong QE (expansive) monetary policy. By committing to raise its inflation target say to 5% (as proposed by Olivier Blanchard) and to buy the distressed sovereign (and bank) debt, the ECB can reduce the real interest rates and and possibily help pushing back the AD curve toward equilibrium 4. This would have additional benefits of taking care of the incoming liquidity crisis of the peripheral sovereigns and banks, as well of inducing a euro depreciation vis a vis the dollar. An expansionary fiscal policy in Germany would also be beneficial.