(From VoxEu)

Many observers of the European debt crisis have embraced the idea that the dangers, in particular the risk of default of Italy, lies in the possibility of “multiple equilibria”. According to this view (1) when economic fundamentals, such as the debt GDP ratio and the primary balance, are neither “sufficiently good” as to guarantee solvency nor “sufficiently bad” to make the country plainly insolvent, then the equilibrium outcome depends on market expectations. In other words, self-fulfilling prophecies may generate opposite and unpredictable outcomes, for the same level of fundamentals. If the market assigns a high probability to a default, it will require a very high risk premium in order to buy governments bonds, making it convenient (or unavoidable) for the government to default, rather than risking strangling the economy to generate the surplus required to repay the loan (bad equilibrium). Whereas if markets are confident in the government ability/willingness to repay, the low yields will generate the right incentives for the government to fulfill the market expectations (good equilibrium). Thus the “credibility is everything”- idea One corollary of this approach, at the European level, is that it is sufficient for the EFSF to be endowed with enough “fire power”, say 3 trillion Euro, in order to prevent a roll-over crisis stemming from a shift in market expectations. Another corollary, relating to the Italian case, is that a sufficient condition for saving Italy is for Mr. Berlusconi, who has lost international credibility, to step down. I argue here that this latter condition, while possibly being necessary at this stage, is unlikely to prove sufficient. Market fundamentals are, unfortunately, still decisive.

THE THEORY

The argument for multiple equilibria has a number of problems. From the standpoint of the theory, it is well known that this result stems from two simplifying assumptions: that each economic agent fully observes all the relevant “fundamentals”, and that everyone has no uncertainty about the behavior of other agents. This allows agents to coordinate perfectly on one or the other equilibrium. Yet, if these assumptions do not hold, then economic fundamentals are back at the center stage, as they unambiguously determine expectations themselves. The equilibrium is again uniquely determined by the strength of fundamentals (2).

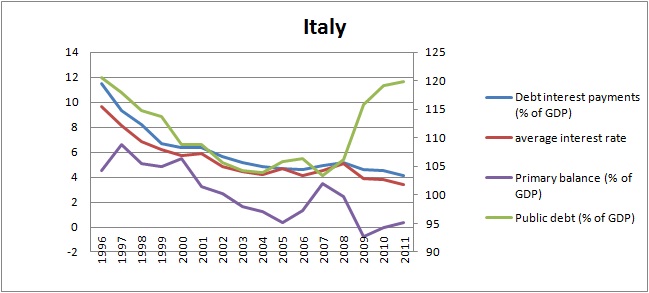

Source: Author’s calculation on Eurostat data

THE EVIDENCE

For the Italian case, the story of multiple equilibria is even less convincing. Figure 1 plots the average interest rate on Italian debt (red line), the ratio of the interest bill to GDP (blue line), the primary balance/GDP ratio (line in purple), and the debt/GDP ratio (green line, right scale) from 1996 to 2011 (the Euro was introduced in 1999). The figure shows how, fifteen years ago, the elimination of currency risk allowed Italy to bring down the average cost of debt from 10 to below 4 percent today, while the interest bill fell from 12% to 4 percent of GDP, allowing a significant improvement of the budget and a strong reduction of the debt ratio, at least until 2004. Note, however that the adjustment effort, represented by the primary balance relative to GDP, gradually weakened over the years. In 2005-6, coinciding with the third Berlusconi government (3), the debt/GDP ratio started to climb back. In 2008-2011, thanks to the crisis and the fourth Berlusconi term, the debt ratio reached its 1996 level, and the primary balance fell in negative territory (and marginally rebounded): 15 years of progress were squandered. What the figure clearly shows is that the puzzle is not that the interest rates are now going up, so far with a limited impact on the interest bill. The puzzle is that interest rates have risen so little and so late, despite the worsening of fundamentals. It is really not necessary to resort to esoteric explanations such as contagion (4) and multiple equilibria in order to explain the recent rise in Italian yields, when the debt/GDP ratio is back to its 1996 level and the primary surplus is about 4 points of GDP lower than in 1996.

CONCLUSION

Until a few months ago, the markets apparently gave too little consideration to fundamentals such as the debt/ GDP ratio and the primary surplus, thinking that Italy’s default and exit from the Euro was unconceivable. As markets now think back, we can expect bond yields to return to the levels of 15 years ago. Mr. Berlusconi’s resignations, while probably necessary at this point, will hardly be sufficient a substitute for a painful and prolonged fiscal adjustment.

Notes (1) Among others see Alesina, A., Prati, A. and G. Tabellini, 1989. “Public Confidence and Debt Management: A Model And A Case Study of Italy,” CEPR Discussion Papers 351

(2) See, for example, Stephen Morris, Hyun Song Shin, 2000, “Rethinking Multiple Equilibria in Macroeconomic Modeling, NBER Macroeconomics Annual, Vol. 15. (2000), pp. 139-161.

(3) See Bloomberg

(4) See my post with Giulio Trigilia on voxeu