by Paolo Manasse and Giulio Trigilia

Berlusconi’s Partito della Libertà is bitterly divided as to what to do with Mario Monti. The doves (ex Christian Democrats) favour a loyal support to Monti, while the hawks (ex-socialists and ex

fascists) are crying shame for the “suspended domocracy” and the “the

bankers coup”. In order to keep his party together, Berlusconi has opted for a time-bomb strategy. Monti, he declared, has

about until June to do the (dirty) job of the necessary reforms, and then Berlusconi’s party will withdraw its

Parliamentary support. The ex Prime Minister has publicly announced a mass (anti-Monti?) party

demonstration in December, followed by the party congress in March-April,

to be followed by new elections. You guessed: Berlusconi is planning a comeback . Now, tax reform, labour

market reform, pension system reform, privatizations, cuts in the cost

of politics, liberalizations of the goods and services markets: that’s a hell of an agenda. How can anyone

think, in good faith, that 6 months can be enough for such an endevour, when Berlusconi took 9 years in power just to look after his own interests?

In

fact, markets believe otherwise.

|

| Authors’ calculations on Data Stream data |

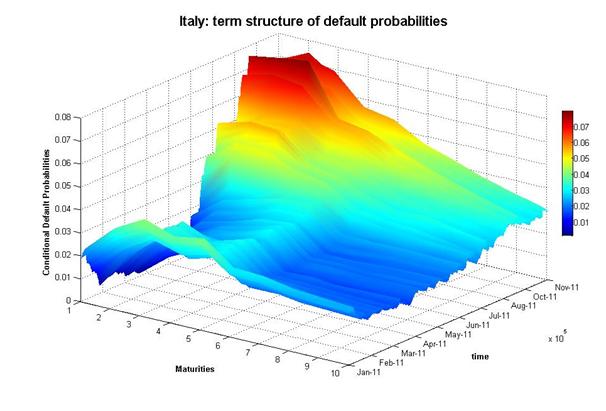

In the Figure above we have used the daily spreads of CDS on

the Italian debt, for maturities ranging fro1 to 10 years. Assuming a

40% recovery rate in case of default, we have calculated the implicit

probabilities of default at different maturities. The figure shows the

conditional

default probability on a contract negotiated at time t with maturity

t+T, p(t, T): This indicates the probability that a default will occurr

between time

t and t+T, conditional on not having occurred before time t. In the

figure, the vertical axis shows the probability p(t, T); the “time” axis on the right

shows

the date when the contract was negotiated t; the “maturities” axis shows the expiry

date of the contract, t+T. The picture gives two types of information. One

can fix a

maturity, say one year, and move along the time axis: this shows the

huge rise of perceived risk on the short end of the maturity spectrum

that has occurred between April and June 2011, when the default probability

climbed from below 2 to above 6%, and again from August to November

2011,

when, with the government paralyzed on budget cuts, it climbed to just below 8%.

Alternatively, one can fix a particulare contract date, say June 2011,

and look the default probabilities at different maturities. By doing so

one can see whether

the contracts negotiated at that particular date incorporate the expectation of

rising or

falling risk, as their maturities rise. What this picture clearly shows

is that, from the beginning of the year, the perceived short term riskiness on of

Italian sovereign debt has quadrupled, rising much more than at the longer horizons. Possibly more

interestingly,

the figure shows that the maturity pattern, as of late, has taken a “hill”-like shape. In other words, markets are

pricing a default

probability that first increases, for maturities of up to 2 years, but then declines progressively (conditional of no default occurring up to 2013).

What financial market are saying is that

it will take Monti at least a couple of years to go past the “harsh

times” : Will Berlusconi listen?